Advanced therapy developers have demonstrated unprecedented proof of platform. So why are valuations so low? And what can be done to ensure life-saving medicines reach rare disease patients in need?

Undoubtably, the biopharma industry has taken a hard hit, with stock prices plummeting and downsizing, which has had an impact on not only smaller biotech companies but also large pharma and associated service sectors. While leading indicators provide hints of a market recovery, forward-looking companies have been strategizing to allocate scarce resources and maximize opportunities for value inflection within the current climate, particularly companies with advanced (cell and gene) therapies. One dominant theme amongst those that are weathering the storm is early investment into diversified portfolios that leverage applicability of advanced therapy platforms across both oncology and non-malignant diseases.

While some have procured partnerships to complement in-house resources and know-how, others have pursued parallel in-house paths to hedge against failure or shifting perceptions favoring one disease area versus another. Whereas oncology provides a rapid path to clinical validation, many programs have struggled to demonstrate commercial value to investors in the face of competitive crowding. Rare, non-malignant diseases, on the other hand, benefit from limited competitive intensity (in most cases) and appear to be driving outsized value for advanced therapy companies within the current climate.

Companies pursuing such bifurcated portfolio strategies have successfully generated clinically-meaningful data in areas of unmet need, creating opportunities for expedited regulatory privileges and accelerated approval timelines. While there’s no denying the role serendipity has played for such fortunate companies, strategic decision-making is critical for creation of opportunities to ‘meet the moment’. At Lumanity, our experienced team of experts have guided countless clients towards successful commercial strategies grounded in an awareness of scientific rationale, historical precedent, and emerging market trends.

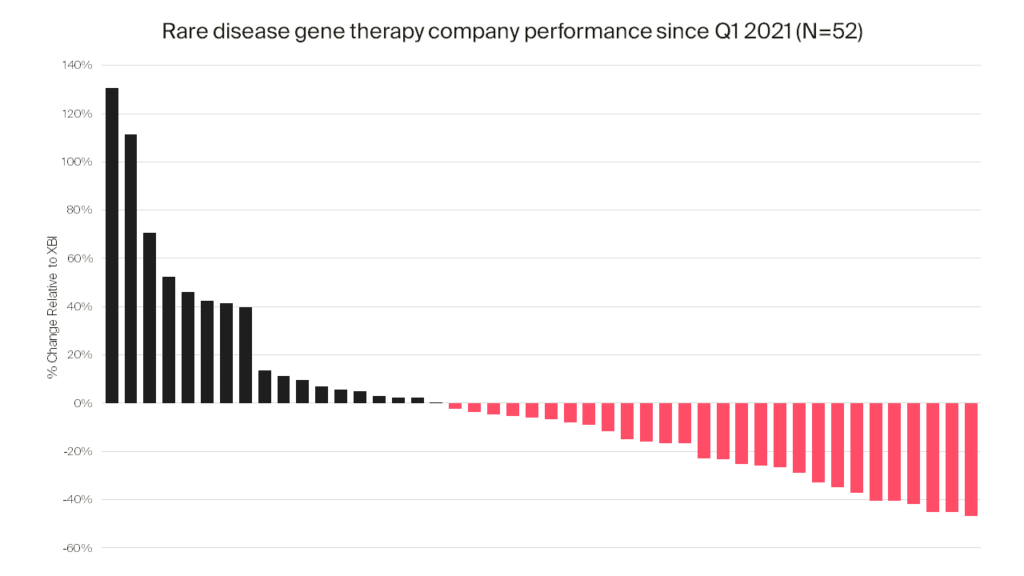

So how bad is bad? The SPDR® S&P® Biotech ETF (i.e., XBI), which represents the biotechnology segment of the S&P Total Market Index (i.e., S&P TMI) has been in a steady freefall for the past several years, losing ~40% since 1Q 2021 (the S&P TMI, by comparison, is down by only approximately 11% over the same timeframe). Advanced therapy stocks have been a particularly hard-hit subsector, with an estimated 60-70% of companies in this category suffering losses exceeding those of the XBI during the same timeframe. The reasons for such losses are beyond the scope of this piece, but no doubt reflect complexities of these modalities, cost of manufacturing, and the inconvenience of administration relative to more established technologies like monoclonals and small molecules.

Against all odds, certain advanced therapy companies appear to be surviving adversity and, in some cases, even thriving under current conditions. While fortune has no doubt played a role, one recurring theme is that of diversification. Though not a new idea, diversification takes on new meaning for companies built around novel and broadly applicable platforms. As in the past, these companies must allocate scarce resources towards pursuit of several high-value applications and programs in parallel, each of which might be met with enthusiasm or skepticism depending on prevailing investor or partner sentiment.

In the advanced therapy arena, unproven gene-editing platforms have been subjected to heavy scrutiny as they are being positioned across both in vivo and ex vivo oncology and non-oncology applications – each field has benefited from exuberant expectations and then suffered from disproportionate skepticism depending on the market sentiments. Examples of companies that have straddled the malignant/non-malignant divide (and been rewarded or punished for one v the other at different times) include the following:

CRISPR Therapeutics (CRSP)

A leading gene-editing company focused on developing transformative gene-based medicines for serious diseases using its proprietary CRISPR/Cas9 gene-editing platform. CRISPR invested early in its oncology pipeline, which has been met with highs and lows. Mid-2022, it terminated its multiple myeloma candidate CTX120 and the dataset that followed sent its stock plummeting. However, CRISPR has come out of 2022 with a $4B market cap, driven largely by its alliance with Vertex pertaining to hemoglobinopathies and type 1 diabetes. This, along with other partnerships, has supported CRISPR’s efforts to move outside oncology and into non-malignant diseases such as diabetes, amyotrophic lateral sclerosis (ALS), Friedreich’s ataxia, sickle cell disease (SCD) and transfusion-dependent beta-thalassemia (TDT). As CRISPR and Vertex near completion of a historic US Food and Drug Administration (FDA) submission with their exa-cel gene therapy, 2023 brings much promise for the gene editing field, SCD and TDT, but also for CRISPR Therapeutics.

Poseida Therapeutics (PSTX)

Has proprietary gene insertion (piggyBAC), gene editing (Cas-CLOVER) and gene delivery (AAV and nanoparticle) technology that has landed them numerous partnerships spanning oncology and rare diseases – ornithine transcarbamylase (OTC) deficiency and hemophilia A. Similar to CRISPR Therapeutics, Poseida also invested early in its oncology pipeline, but has since diversified into non-malignant diseases. While not all of its deals have been successful, its partnership with Takeda is certainly paying off: for example, these two companies are on course to develop six in vivo gene therapy programs with an added option for two more where Poseida drives the research entity and Takeda supports manufacturing and commercialization. Perhaps this is the mechanism by which Poseida has managed to escape downsizing and workforce restructuring?

Intellia Therapeutics (NTLA)

Also has a leading ex vivo treatment for hemoglobinopathies partnered with Novartis. However, Intellia established first-in-human proof of concept for a liver-targeted non-viral lipid nanoparticle (LNP) delivery of a two-part genome editing system: guide RNA specific to the disease-causing gene and messenger RNA that encodes the Cas9 enzyme. The initial in vivo success of knocking out transthyretin (TTR) for the treatment of ATTR amyloidosis drew a partnership with Regeneron and opened the opportunity to build a pipeline of one-time durable treatments for diseases (such as hereditary angioedema, alpha-1 antitrypsin deficiency, hemophilia A/B) that have already been validated by chronic small interfering RNA (siRNA) administration and silencing of pathogenic gene expression developed by pioneers like Alnylam and Ionis.

Verve Therapeutics (VERV)

Has built a portfolio utilizing their proprietary GalNAc-lipid nanoparticle delivery technology to draw partnerships with Beam Therapeutics, supporting their two base editing programs, and Vertex Pharmaceuticals, for a future gene editing therapy in an undisclosed liver disease. Unlike others highlighted above, Verve pursued non-malignant disease targets early on and steered clear of the overcrowded oncology market. Whether serendipitous or insightful thinking, Verve is continuing to pursue strictly non-malignant diseases (heterozygous familial hypercholesterolemia, atherosclerotic cardiovascular disease, homozygous familial hypercholesterolemia) as they push into 2023 with upcoming milestones. In mid-2023 Verve is expected to provide an update on its response to the VERVE-101 clinical hold and late-2023 will provide the first clinical data that could de-risk base editing.

To be clear, the examples cited above are not necessarily outperforming of late. But each managed to capture value from one or more programs within portfolios that span both oncology and non-oncology applications. It may not always be pretty, but many of these companies appear to be here to stay, thanks in no small part to their ability to successfully diversify applications stemming from the same or related platforms and corresponding domain expertise.